The signs that Europe really is doomed – and taking Britain down with it

When Tom Crotty joined Ineos in 2001, the petrochemicals giant was in the middle of a European buying spree.

Crotty joined after the refrigerants division he ran at ICI was snapped up by Sir Jim Ratcliffe’s growing industrials empire, part of a string of deals that culminated in the $9bn (£6.7bn) acquisition of BP’s chemical assets just a few years later.

That deal was so large that Ineos’s finance director had to phone the Bank of England to confirm the transaction was real.

Back then, Europe was booming. “There was a lot of expansion,” recalls Crotty, who has been in the chemicals industry since graduating in 1979 and is now a senior director at Ineos.

“A lot of the new developments, in terms of processes and products, were being made there and were resulting in manufacturing being built in Europe.”

The year 2001 was significant for another reason. China joined the World Trade Organisation (WTO), becoming its 143rd member after a 15-year diplomatic struggle.

But fast-forward two decades, and companies like Ineos are struggling in Europe.

Cheap imports from China are hurting – but it’s not just that. The bloc’s high energy costs and what founder Ratcliffe has described as “bonkers” rules that threaten to punish the company for going green are also crippling industry.

The dynamism that Crotty recalled at the turn of the century is long gone, and not just in the chemicals sector.

Across investment, company creation, research and development (R&D) and more, Europe is lagging behind the world’s superpowers – China and the US.

b’

‘

Too many of the Continent’s best and brightest are fleeing abroad. In many cases, Brussels is responding to this crisis in the only way it knows how: regulation.

“It has been quite a long time since Europe has been in that world-beater category,” Crotty laments.

It may be too late to stop the rot, with only a full-blown crisis able to shake the bloc out of its slumber. And if Europe’s decline continues, the pain will wash up on Britain’s shores too – even after Brexit.

“If it keeps going the way it’s going… many of those countries will not be viable countries any longer,” the US president told Politico.

Trump was referring to an EU leader’s approach to immigration – but to some observers his comments rang true economically too.

“When you look at the US, most of their top companies didn’t exist 30 years ago,” says Xavier Niel, a French telecoms billionaire. “When you look at France, all of ours already existed back then.”

He believes the Continent has become stuck, just as others have pulled ahead. A bloc that at its peak drove more than a quarter of world output now drives roughly a sixth.

Emmanuel Macron would like to blame China. The French president used a visit to Beijing last week to brand its economic policy “unbearable” for the EU, after the world’s second-largest economy posted its first ever $1tn trade surplus with the rest of the world.

The French president warned that Europe now faced a “life or death” moment as he accused Beijing of “hitting the heart of Europe’s innovation and industrial model”.

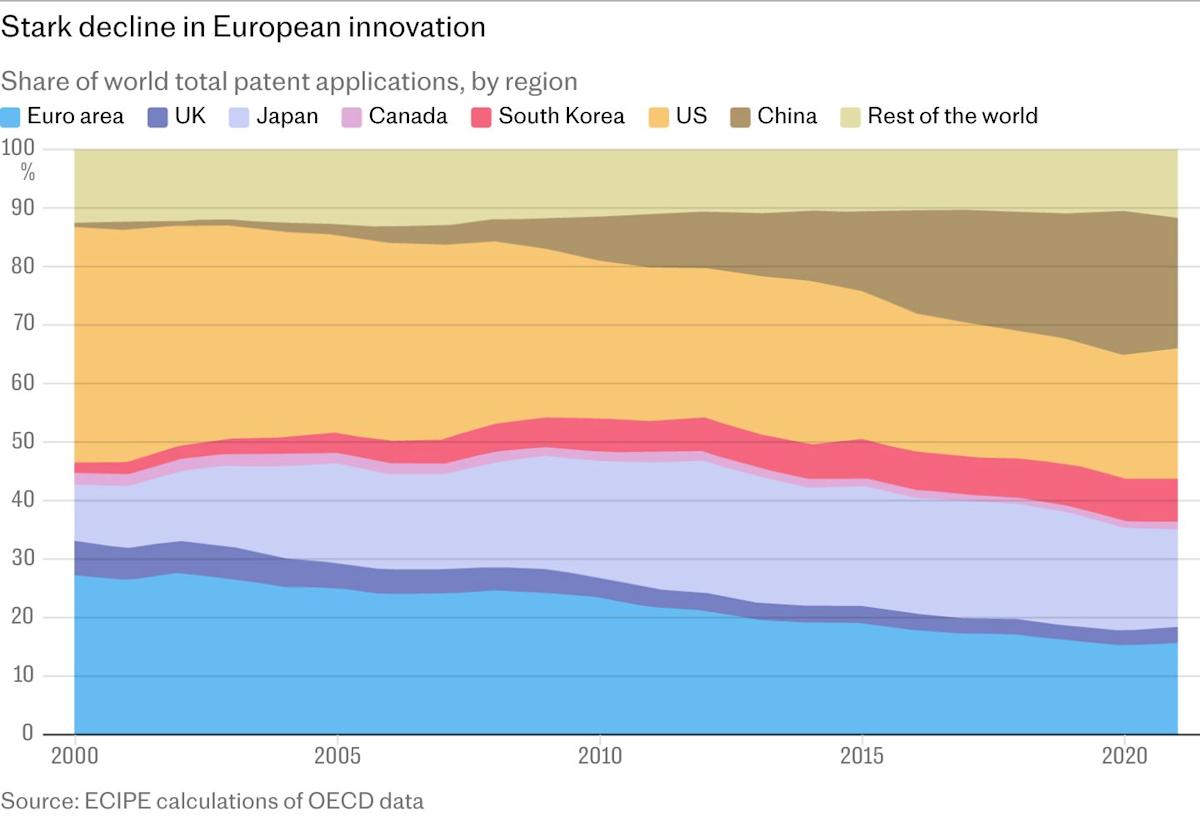

But Europe’s decline is also of its own making.

Once the second-most innovative region behind the US, with 27pc of global patent applications in 2000, the eurozone had slipped back to fourth place by 2021.

“You’ve now got a situation where China is filing more patents than Western Europe and the US put together,” says Crotty. “That’s a massive change over a period of 20 years.”

The EU undoubtedly missed the last great wave of innovation in the rise of the internet. Leaders in Brussels now claim to be looking forward into the industries of the future – AI, robotics, digital services and defence.

But when Mario Draghi, the former prime minister of Italy and ex-head of the European Central Bank, wrote his landmark report on EU competitiveness last year, he painted a bleak picture of the bloc’s prospects in these areas.

“Europe is stuck in a static industrial structure with few new companies rising up to disrupt existing industries or develop new growth engines,” he warned.

Companies in Europe struggled to rival the size of those in the US or China because of a barrage of red tape and sky-high energy prices, his report warned.

b’

1412 EU pays a premium for electricity prices compared to China and the US

‘

Draghi recommended the bloc increase spending by €800bn (£703bn) per year or face being left behind by the US and China.

He called for policymakers to invest in innovation, make European mergers easier, cut red tape and make it easier to do cross-border business, particularly in financial services.

The report draws a telling parallel.

In the past two decades, US spending on R&D – the tinder of innovation and productivity – shifted from the automotive and pharma industries in the 2000s to software and hardware companies in the 2010s, and then to the digital sector in the 2020s.

Yet over all that time, Europe’s spending has remained stuck in the automotive sector – eking out marginal productivity gains instead of chasing high-growth frontiers.

The crown is also slipping from Europe’s pharmaceutical sector. Of the top 10 best-selling biological medicines in Europe in 2022, just two were marketed by EU companies. Six came from US-based companies.

Europe’s drugmakers aren’t spending enough on R&D, and they’re not alone. European companies spend a collective 2.2pc of the bloc’s GDP on R&D. The US figure is 3.5pc, and South Korea is touching 5pc.

But problems run deeper than big businesses resting on their laurels.

The start-up culture is struggling too. No company has been set up in the EU in the past half-century that now has a market capitalisation of more than €100bn. In that period, six US companies have been established that now have a valuation of more than €1tn.

“We don’t have enough entrepreneurs in Europe,” says French billionaire Niel. “The issue isn’t talent – we have plenty. The issue is that not enough European young people wake up one morning thinking, ‘I’m going to build this massive company that’s going to change the world’.”

Nicolai Tangen, boss of the world’s largest sovereign wealth fund in Norway, says American investors have noticed.

“I’ve just come back from the US, I spent a month there. I met with 70 [chief executives], and the overall impression is that there is not so much happening in Europe,” he says.

“Regulation is a big part of it, but it’s a lot of factors: regulation, innovation, competitiveness, all these things.”

Tech companies are grappling with the Digital Services Act, the Digital Markets Act, the AI Act, the Data Act and the Cyber Resilience Act – some of which have evoked sharp hostility from Trump’s White House.

Donald Trump, pictured with Ursula von der Leyen, has called Europe’s Digital Services Act an ‘attack’ on US tech giants – Andrew Harnik/Getty Images

In the tech space alone, the Bruegel Institute has tallied up more than 100 laws and regulations administered by more than 80 different agencies.

“Europe doesn’t have an innovation problem, it has a regulation problem,” Niel says. “If I want to build an AI company today, I’ll go where it’s easier in terms of regulation. And right now, that’s not Europe.

“Europe always over-regulates, while in China regulation is virtually non-existent and the US is trying to lighten theirs. Innovation is unpredictable by nature. If we regulate too soon, we risk slowing everything down.”

Some of the EU’s tech laws are now being reconsidered or wound back, as businesses chafe under requirements not imposed on companies elsewhere.

But the damage is already done. Between 2008 and 2021, almost one third of the “unicorns” founded in Europe – start-ups that went on to be valued at over $1bn – relocated abroad, mostly to the US.

It’s not just technology either. The EU has been busily padding out its rulebook elsewhere too – with directives aimed at enforcing environmental, social and governance (ESG) norms on companies.

The Corporate Sustainability Due Diligence Directive, the Regulation on Deforestation-Free Products, the Corporate Sustainability Reporting Directive and the Forced Labour Regulation have all landed since mid-2023.

Claudio Irigoyen, global chief economist at Bank of America, says this regulation-first attitude has put Europe on the path of secular decline.

“The AI revolution is happening in the US and China under completely different regimes. It is not happening in Europe,” he says.

“There is no development, but they are already discussing how they will regulate it. This mindset needs to change.”

Europe’s canary in the coal mine came from one of its most modern, future-facing industries: solar power.

At the turn of the century, Germany was a world leader in both developing and making the photovoltaic (PV) cells that turn sunlight into electricity.

The German government passed a renewable energy law in 2000 that encouraged investment, spawning an industry that quickly employed 150,000 people.

Communist central planning – backed by a bazooka of state subsidies – built a whole PV supply chain in less than a decade.

As the Chinese industry went into subsidy-fuelled overdrive, exports began to flow. By 2010, European-made solar panels were being priced out of their own market.

Brussels levied tariffs in 2012, but it was too late. European manufacturers started throwing in the towel.

The problem only got worse. Beijing kept the subsidy tap on, creating a supply glut. In the early 2020s, by which point China controlled close to 90pc of the world PV market, prices halved again.

China built a solar panel supply chain in under a decade, and now dominates the industry – STR / AFP via Getty Images

The US put tariffs up, sending all that cut-price surplus flooding into Europe. In the past 18 months, another half-dozen European manufacturers have rolled down the shutters. Brussels has scrambled to put the last few players on financial life support.

Now the amber light is flashing for the car industry.

Chinese giant BYD and its heavily subsidised peers have tightened their grip on their domestic market, and are pushing harder into the wider world at extremely competitive prices.

You could argue that the EU was a helpless victim in all this. But China’s ability to seize the initiative in the car market in part reflects the weakness of European car makers that have failed to keep innovating.

Chinese customers, who largely value passenger over driver experiences, have shunned European models that have shorter wheel bases and a lack of entertainment.

As a result, the EU became a net importer of cars from China for the first time last year. Chinese brands sold almost twice as many vehicles in Europe in the year to September – even after Brussels hit them with tariffs of up to 45pc.

b’

1412 EU now imports more cars from China than vice versa

‘

Legally binding net zero targets that enshrine into law a pledge to eliminate carbon emissions from supply chains have also hobbled industry.

Crotty at Ineos says Europe is shooting itself in the foot with these policies.

“A huge proportion of our energy costs in Europe are self-inflicted because they are a combination of levies and tariffs on power and power transmission, plus CO2 taxation that does not exist anywhere else in the world.

“Trump has eliminated CO2 taxation in the US. There is no CO2 taxation in China. There is no CO2 taxation in the Middle East. But we’ve got it in Europe. And why is it there? It’s supposed to be there to eliminate emissions. Does it do that? No, it doesn’t. Because all it does is it means you kill your European industry.

“So the product that industry was making is now supplied from China at much higher rates of CO2 emissions, not only because it has to be transported halfway across the world, but because they’re using dirtier processes that emit a lot more CO2.

“So the whole purpose of these CO2 taxes, which was to reduce CO2, has had the opposite impact. It’s lost jobs and it’s increased CO2.”

China’s wrecking ball won’t stop at solar panels, chemicals and cars. Europe still dominates China across a range of key exports including commercial vehicle engines, tractors valves and vacuum pumps. But once again, Beijing is catching up.

Analysis by Goldman Sachs of 32 capital goods where Europe still leads China in terms of exports shows the Continent’s share has declined from 56pc of all global volumes in 2005 to 44pc today.

China, meanwhile, has increased its market share in these categories – which also includes bearings and escalators.

Very little is safe from Chinese competition. The pandemic and Ukraine war created a tectonic shift in energy costs, with China one of the main beneficiaries of cheap Russian oil while Europe’s energy costs soar.

“Comparing 2024 to 2019, China has gained share in most of the product categories while at the same time Europe has been losing,” the analysts noted.

There is one category where Europe’s market share has increased over the past five years: toilets. At least not everything is going down the pan.

Can anything break Europe out of this malaise?

The Continent loves a good crisis. Jean Monnet, the man dubbed “the father of Europe”, famously declared the bloc would be “forged in crisis, and will be the sum of the solutions adopted for those crises”.

There’s a general agreement that Europe still has reservoirs of talent, capital and entrepreneurship that could underpin a renaissance of growth and productivity.

Europeans have some of the highest savings rates in the world – almost 40pc of household wealth is languishing in bank deposits. This locks up capital that could be funding growth.

Veteran investor Lord Jim O’Neill is one of the optimists. “There’s a difference between size and wealth,” says the former government minister and chairman of Goldman Sachs Asset Management.

“Some of the world’s wealthiest countries are European and are still seeing their wealth increase.”

Those who say Europe is already eating China’s dust miss this point, he says.

But Lord O’Neill warns that leaders are often more fixated on the idea of Europe than with pushing through policies that could return the bloc to its status as an economic powerhouse.

b’

1412 Notable decline in UK and eurozone productivity

‘

The pace of reform in France is “staggeringly laughable”, he says.

“The way Europe behaves is that it takes really crisis events to force change.”

Bank of America’s Irigoyen, who worked at Argentina’s central bank in the wake of the country’s largest ever default, says the bloc needs shock therapy of the kind being pursued today by Javier Milei in Buenos Aires.

There is precedent. Spain and Greece are now among the bloc’s fastest growing members after taking some tough medicine when both ran out of cash.

Unfortunately, voters across Europe are unlikely to swallow such tough medicine.

“When you have 3pc inflation, you’re not going to [get the same reaction],” he says. “So politicians don’t get rewarded by doing the right thing to avoid problems in the future.

“That means unfortunately, Europe needs to see more pain in order for politicians to perceive that they have a mandate to do what needs to be done.”

O’Neill says Draghi has already written the blueprint for change. Politicians just need the mettle to follow through.

“I know some people of my generation who sit in the middle of all of this in Europe, and they pray there’s going to be a crisis so they can do it all.”

Whether Europe’s future is slow-motion stagnation or cathartic crisis, even a post-Brexit Britain will struggle to avoid the consequences.

More than half of Britain’s goods trade is still with the EU. The UK is the bloc’s third-biggest customer after the US and China.

It’s part of the reason why David Lammy signalled that rejoining the customs union would be good for Britain’s economy, claiming it was “self-evident” that Brexit had inflicted damage.

Labour was forced to deny it was pursuing such a plan, though Sander Tordoir, chief economist at the Centre for European Economic Reform, says Britain is likely to continue pegging its fortunes to its nearest neighbour.

The UK has been trying to go beyond the EU with its “Global Britain” strategy, but in a world where global markets are under pressure, “the prospects for that look a bit more dim to me”, he says.

Brexit may have given Britain a lifeline to avoid Europe’s economic misfortune – Peter Marshall / Alamy Live News

Kevin O’Marah, of Zero100, a supply chain consultancy, is no fan of Brexit but acknowledges it may have opened up opportunities to forge a different path to the bloc.

He reckons the UK could potentially redefine itself as a “middleman” economy, a convenor of capital, services and ideas.

“I don’t blame Britain for saying to the EU, ‘Listen, you guys are just like sitting on your hands over there, you’re not doing anything’. There’s a governance problem in the European Union that is so severe that Britain quit,” he says.

But he’s unsure the Starmer Government is taking the right tack. The potential of Brexit won’t be realised, he warns, if “you tax the profits of those businesses so heavily that they say, ‘Forget it, I’m not going to bother.’”

“You’ve got a bit of a problem right now in the UK with a tax regime and an attitude to intellectual-property-based wealth creation that is causing people to say: ‘Why bother?’ You’ve got to let businesses thrive.”

Labour is considering the prospect of reheating its formal ties with the EU market, but Tordoir says this will both “reopen all the old discussions and trade-offs around Brexit” – not just in the UK, but in the EU.

He points out that despite France, Germany and Britain working in lockstep on Ukraine, the French helped scupper British participation in the bloc’s SAFE military funding package.

Sir Keir Starmer baulked at Brussels demands for a €6bn entry fee to participate in the fund, which had echoes of the UK being asked to bankroll the EU budget by the back door.

“That had a clear economic dimension. So some of the old tensions are still there, simmering,” says Tordoir.

Crotty says Ineos remains in Europe, but is firmly in survival mode.

“We believe that if we are the lowest cost and the most efficient, then we’ll still be here while others have fallen by the wayside.”

In the European industrial landscape of today, he says, there’s only one option: “Our strategy right now is to be the last man standing.”