Don’t Look – But We Might Be on the Brink of a Market Breakout

For the better part of three plus years, most small carriers and owner-operators have felt like they’ve been grinding uphill in soft dirt. Rates fell, truckload volumes cooled and tender rejections disappeared. All while new authorities flooded in and every time it looked like things might turn, something else pushed it back down to a harsh reality.

But when you zoom out and look at the data—not emotions, not social media, not one hot lane on a Tuesday morning—there are a few signals starting to line up.

This is not a guarantee. It’s not “the market is back.”…….

It is simply this: several key indicators are shifting at the same time. And when that happens, you pay attention. Let’s walk through it in plain language.

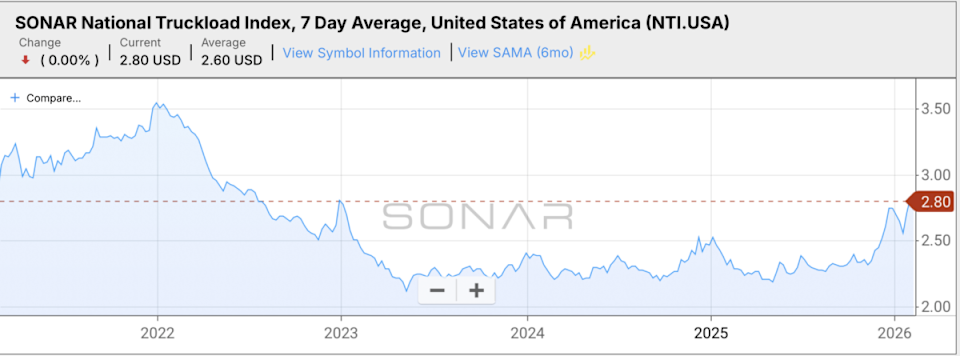

Chart: SONAR, NTI.USA. Spot rates collapsed from 2022 highs and spent most of 2023–2024 near the bottom. The recent climb toward $2.80 suggests pricing pressure may be slowly shifting back toward carriers.

Over the past few years, the SONAR National Truckload Index (NTI) tells a clearer story. We peaked in 2022 above $3.50 per mile on a 7-day average. Then the long decline set in. By 2023 and into 2024, spot rates settled into the low $2.00s.

Right now, NTI is sitting at $2.80, a high we haven’t seen in ages it seems. That matters, a lot…

We are no longer scraping along the bottom. We’re not back to the COVID highs either. But what we are seeing is stability with upward pressure building. The recent move up toward $2.80 suggests the floor may be firming.

When rates stop falling and begin stair-stepping upward—even slowly—that’s usually the first stage of a market shift.

Is it a breakout? Not yet. Is it different than mid-2023? Absolutely.

Chart: SONAR, OTVI.USA. Freight volumes have come down from their peak but are no longer in freefall. Stabilizing demand combined with shrinking capacity can tighten markets over time.

The Outbound Tender Volume Index (OTVI) measures how much freight shippers are trying to move electronically through contract tenders.

At its peak in 2021–2022, volumes were strong. Then they declined sharply through 2023. Right now, OTVI is around 10,110, slightly below its historical average of 11,731.

What does that mean in real terms? It means freight demand isn’t booming—but it has stopped collapsing. And in markets like trucking, stabilization often comes before tightening.

If volumes hold steady while capacity continues to shrink (and we’ll talk about that next), the balance shifts. Not overnight but gradually.

The Outbound Tender Rejection Index (OTRI) may be one of the most important indicators in this entire conversation. This is simply put, the amount of freight contracted carriers “reject” due to better opportunities on the spot market.

For most of 2023, OTRI lived in the basement. Carriers were accepting almost everything because there wasn’t enough freight to go around.

Now OTRI is sitting at 13.40%, well above its recent averages.

When rejection rates rise, it means carriers are beginning to gain options. They’re declining lower-paying contract freight in favor of better opportunities—often in the spot market. This is how spot rate momentum builds.

Chart: SONAR, OTRI.USA. Rejections are climbing. Carriers are beginning to push back instead of taking every load. That shift in leverage often leads spot rates upward.

Now let’s talk about capacity.

The Carrier Details Net Changes in Trucking Authorities (CDNCA) chart shows net changes in active authorities. For the last few years, we saw waves of new entrants flood into the market. Now we’re seeing net contraction. In plain English: more carriers are leaving than entering.

When capacity shrinks while freight stabilizes, the market tightens. And tightening markets lead to higher prices. It doesn’t happen overnight. It happens gradually, then suddenly.

Chart: SONAR, CDNCA.USA. The flood of new carriers has slowed to a crawl and capacity is contracting. When trucks leave the market and freight holds steady, pricing pressure builds upward.

The TRAC map shows lane-level rate momentum. Blue markets indicate above-average rate increases. Red markets show decreases.

Right now, the country is largely shaded blue. That doesn’t mean every lane is hot. It means more outbound lanes are showing rate strength than weakness in comparison to a few days ago, and it is not weather driven like the past few storms would indicate.

When rate increases become widespread geographically instead of isolated to a few markets, it signals broader tightening of market conditions, in February of all months which is usually slower.

Chart: SONAR, Van Spot Market Conditions. More outbound lanes are showing rate increases than decreases. When momentum spreads across regions, it suggests a broader shift rather than isolated hot markets.

Here’s the cautious part. Markets don’t ring bells at the bottom and they for sure don’t send party invitations before they turn.

But historically, breakouts happen when three things line up:

Rates stabilize and begin climbing.

Rejections increase.

Capacity contracts.

Right now, all three are happening simultaneously. That does not guarantee a surge but itt does suggest the long bottoming process may be ending.

Could volumes dip again? Yes. Could macroeconomic conditions slow freight? Absolutely. Could fuel volatility disrupt margins? Always.

But the data is no longer pointing downward. It’s pointing sideways to slightly up. And that’s a major change from where we’ve been.

The carriers who survived the downturn have leaner operations.and lower overall costs in some cases. If rates lift meaningfully, those operators will see margin relief quickly. The ones who were barely holding on operationally may still struggle even in a rising market.

We are not declaring a boom, we are not forecasting $3.50 national spot rates next month.

We are simply observing this:

That combination has historically preceded market tightening. The next 60–120 days will tell us whether this is a head fake or the early stage of a breakout. For now, stay plugged in, stay cautious but don’t ignore what the data is saying. Something is shifting.