Chinese Savers Have $23 Trillion and Few Options Beyond Stocks

(Bloomberg) — Chinese households are tiptoeing back into equities, driven in part by a stark reality: Almost nothing else looks worth buying.

The CSI 300 Index has surged more than 25% since its April lows, fueled by enthusiasm over artificial intelligence and Donald Trump’s softer rhetoric on China. But other asset classes — from wealth management products to money-market funds — remain stuck in a years-long slump.

Most Read from Bloomberg

That’s reviving an old bull market mantra: there is no alternative to stocks. The idea that China’s small investors will shift a chunk of their $23 trillion savings pile to the stock market is a tantalizing one for global firms, who are showing signs of returning after years on the sidelines.

“The pressure to save is fading,” said William Bratton, head of cash equity research in Asia Pacific at BNP Paribas Exane. The huge savings pool is one reason his firm is “structurally positive” on China’s stock market, he said.

So far, retail investors haven’t driven the rally — local institutions and foreign inflows have, according to Goldman Sachs Group Inc. But small investors are central to the bull case. JPMorgan Chase & Co. sees about $350 billion of additional savings flowing into stocks by the end of 2026.

Here are some of the other places Chinese investors could put their money — and why they probably won’t want to.

Cash

Cash is still king for China’s nation of savers, but the crown has lost its shine.

The nation’s four biggest banks offer returns of around 1.3% for five-year savings accounts, down from around 2.75% in 2020, according to state media reports. Demand deposits, which savers can withdraw at any time, pay just 0.05% per year.

Returns on money-market funds have also crumbled. The giant Tianhong Yu’E Bao fund, which manages around $110 billion of assets, returns around 1.1%. That is less than half what the fund’s investors earned at the start of 2024.

Bonds

Bonds aren’t doing much better. Investors holding Chinese government debt have faced more monthly losses than gains this year so far, according to a Bloomberg gauge of total returns.

Falling bond prices are accompanied by higher yields, which should ultimately make bonds more attractive to investors. But a resumption of tax collection on interest paid by the government or financial institutions has given investors yet another reason to put their money elsewhere.

The yields available also remain unappealing in historical terms, even after the recent rise. Benchmark 10-year government bond yields now hover around 1.80%, well below the five-year average of 2.58%.

Property

Property was for years the default option for Chinese investors looking to generate investment returns, but after a four-year downturn there are few signs of buyers returning.

Many families already own more than one home, reducing potential demand. President Xi Jinping’s repeated mantra that “houses are for living, not for speculation” has served as a warning to would-be investors. Property developers, struggling to finish previously sold homes, have also dented confidence.

Roughly 58% of the country’s household wealth is in real estate, down from 74% in 2021, according to research from China International Corporation Corp. Stocks and other high-risk financial assets account for 15% after jumping six percentage points over the same period, the firm estimates.

Wealth Management

Wealth management products have long been a popular investment for investors. But average annualized returns for both pure fixed-income and mixed strategy wealth management products are now under 3%, according to data tracker PYStandard, which analyzed returns from recent quarters. That cements a more than two-year downturn in what investors can earn from WMPs.

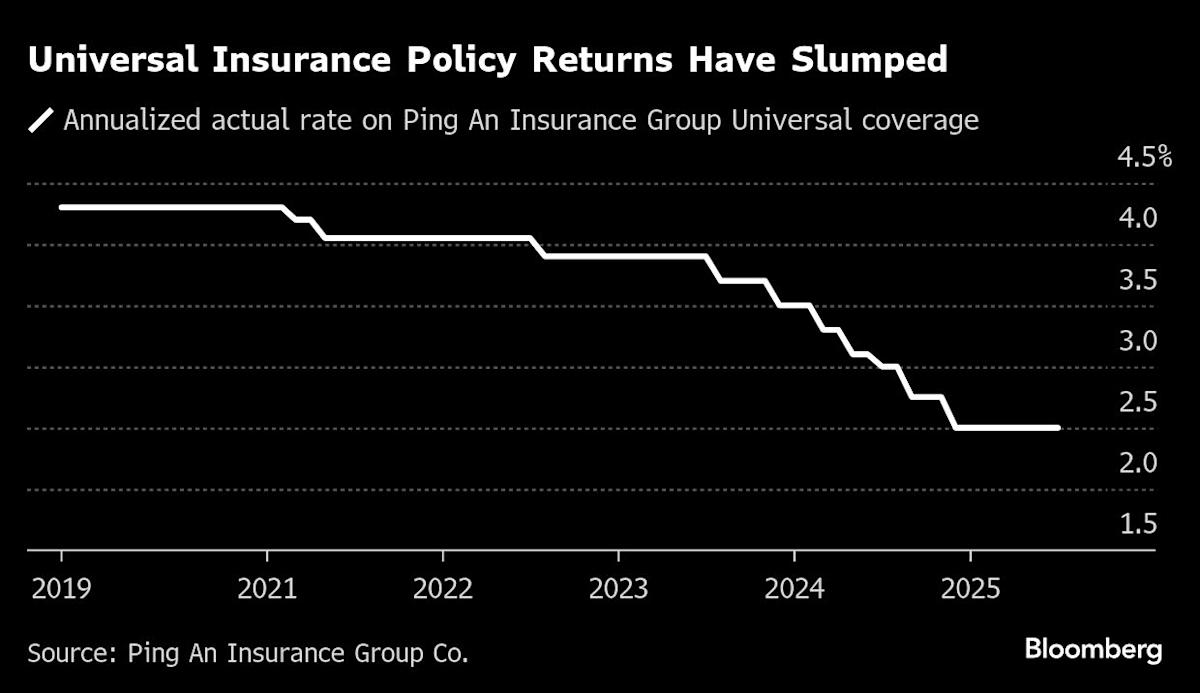

Insurance

Life insurance products, a popular form of investment in China, have gone in the same direction: The annualized rate of return on some of Ping An Insurance Co.’s universal policies has slumped to 2.5% from 4.3% before the Covid-19 pandemic, according to its own data.

Still, if there is no alternative to equities — what about stock markets elsewhere?

Chinese investors have in past years made bets on other markets, including finding ways to get exposure to the Magnificent Seven technology stocks in the US. But capital controls are a big hurdle. Local investors aren’t permitted to convert more than $50,000 into foreign currencies each year, and funds that offer access to foreign markets are subject to their own quotas.

They also face a heavy tax burden, with local officials imposing a 20% levy on income from overseas investments.

That means Chinese investors face a choice between a plethora of easy options at home that are largely unattractive, and a few eye-catching assets overseas that aren’t so easy to buy. Analysts are guessing they’ll take the middle ground — and keep ramping up their bets on local stocks.